In the FINDER project, with a broader scope, we investigate how the continuously increasing pace of digitalization shapes the collaborative innovation of firms. Such innovative trajectories do not necessarily pan out in a linear fashion. In fact, they can even hold the potential to induce strategic reorganization of firms’ organizational form (The Centre for Organization Restructuring hosted by Radbouds’ Institute for Management Research bundles expertise on this field). Such change can have different antecedents either originating in an approach of long-range planning or a firm’s threat of survival. In all cases, however, one needs to acknowledge that such a strategic reorganization holds advanced interdependencies to their collaborative networks.

FINDER, as a project by Radboud University & Atos, therefore hosted a two-day symposium to examine the influence of Atos’ strategic reorganization of its vertical Financial Services & Insurances (FS&I) on its innovative collaboration network.

In order to make full use of the intersection between academia and practice, the symposium was divided into two days to provide the necessary space to explore both perspectives. The first day provided various intra-organizational angles onto Atos transformation to transmit a holistic picture. Connecting the inputs of the first day with the ESRs focal points of research on the second day delivered new perspectives rooted in research on said transformation.

Together with members of the Atos Scientific Community, the Atos Scaler program, and the FS&I leadership team we fruitfully discussed how digital technologies necessitate an intra- and entrepreneurial handling of digital technologies. The focus was on the combination of large (corporates) and small (FinTechs) organizations in the Financial Services Industry and upper management’s role as policy-makers to facilitate new ventures. More specifically there were four different topics discussed on the second day:

Jonas Röttger:

Firms communication in M&As and its effect on the stock market

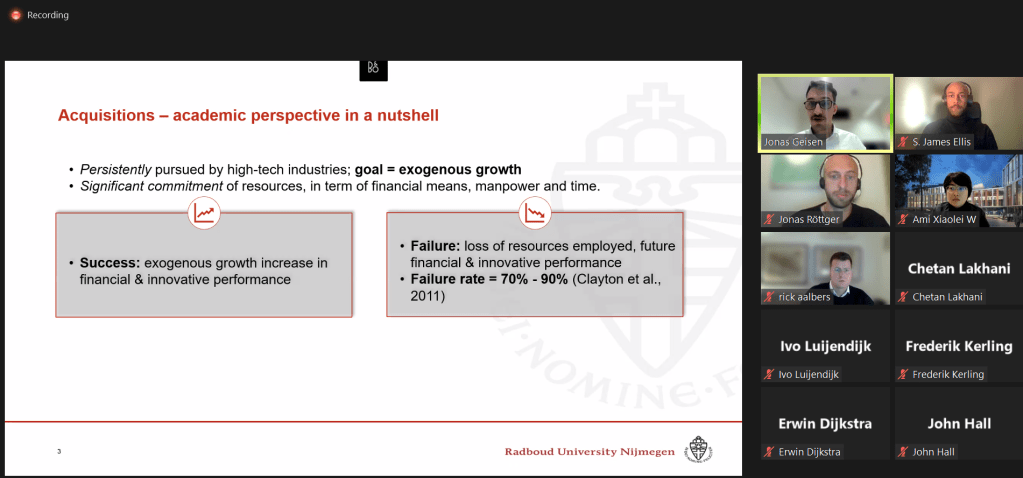

Jonas Geisen:

Dancing to the rhythm: the dynamics of acquisition motive on serial acquisition

S. James Ellis:

Ecosystem dominance – three approaches to emerge on top

Ami X. Wang:

Incumbents and Entrepreneurial ventures In The Digital Era

Highlighted by the interest of the participants in the insights it becomes apparent that there is a demand for diffusion and direct application of scientific knowledge. This symposium and FINDER, due to its unique feature of intersecting academia and industry, serve this purpose through research that provides meaningful insights to understand and foster innovation for and applicable by practitioners. We are happy to share that this symposium, with its collaborative format and fruitful discussions with Atos, successfully delivered on FINDERs purpose of an ambilateral diffusion of knowledge achieving an incremental impact for both academia and practice. This becomes more visible in its outcome as the practitioners provided the ESRs with hands-on input for their research while the ESRs presented new perspectives derived from research for Atos practitioners.

– Jonas Geisen, ESR