Another milestone from the FINDER project—a fresh publication in the FT50-listed journal Research Policy, highlighting the caliber and impact of research emerging from our program.

The article, titled “Middle managers at the crossroads: Navigating legitimacy tensions in pursuit of radical innovation in nascent ecosystems”, is based on the Atos Case, a central pillar in the FINDER Fintech scoping, and is coauthored by FINDER’s recent PhD graduate Dr. James Ellis, alongside Saeed Khanagha, Rick Aalbers, and Philipp Tuertscher, all FINDER academic supervising crew.

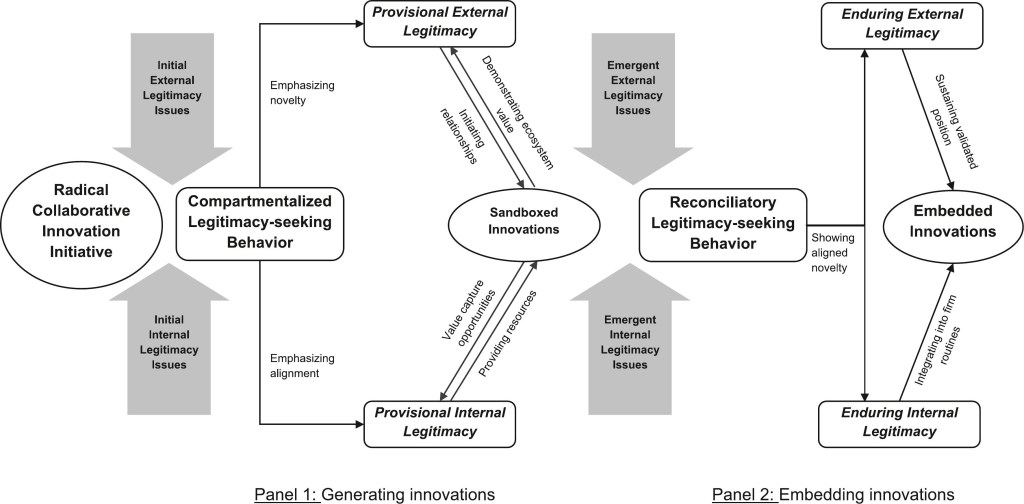

What’s it about? This longitudinal case study dives deep into the role of middle managers as strategic orchestrators in digital innovation ecosystems. Using a rich case from Atos, the authors unravel how these managers navigate the legitimacy tensions between internal organizational expectations and external ecosystem demands—particularly while working with fintech startups to drive radical innovation.

At the core of the study: How can a legacy IT services giant like Atos become a central orchestrator in the fintech space? The authors trace how middle managers within Atos sought to reposition the firm—not just as a service integrator in banking, but as a hub connecting fintech start-ups and financial institutions to co-create radical, collaborative innovations.

Through a rich longitudinal field study, the paper examines the strategic communication and action patterns managers used to gain trust and alignment within a nascent and high-stakes ecosystem. It highlights how discursive and performative actions help managers continuously adapt their strategies to evolving stakeholder landscapes, offering new insight into the messy, dynamic, and high-stakes world of collaborative innovation.

(Diagram illustrating the legitimacy-seeking behaviors central to middle managers in fintech innovation ecosystems)

Why this matters:

Sheds light on the strategic agency of middle managers in uncertain environments

Offers a framework for understanding legitimacy-seeking behavior over time

Bridges firm-level and ecosystem-level adaptation under fintech dynamics

Reinforces FINDER’s mission of exploring future-oriented, digital innovation in practice

With that, this publication stands as a testament to the impact and relevance of the ongoing FINDER research and as FINDER crew we couldn’t be prouder of James and the coauthoring team for pushing the boundaries of management scholarship. More to come!

Just a few days ago, my second Academy of Management conference ended. The timing couldn’t be more fitting, as I’m gradually wrapping up my industrial PhD trajectory within the FINDER project. As my contract officially concludes at the end of this month, this conference served as a reflective milestone, tying together much of the work and learning from the past years.

This time, I had the opportunity to present the paper we are developing on sequential strategies to conduct acquisitions and divestitures. The project has been quite exploratory due to two key novelties for me. First, while the sequence analysis approach has already been established by prior work, we advanced it by shifting to an evolving rather than static perspective. Second, the large volume of data required to model and assess these strategies presented a rewarding coding and computational challenge.

I was happy to see that the paper was received favorably by both the initial reviewers and the AoM session (my thanks to Jan-Michael Ross, Dmitry Sharapov, and Manish Popli for their insights). In a field where a considerable amount of time passes between the first creation of an idea and its external feedback, this response was both validating and energizing. It offers a clear direction on how to further refine the paper which I will implement jointly with the much appreciated support of my supervisors Rick Aalbers and Killian McCarthy.

Want to read more? Please reach out to receive this FINDER enabled working paper: With or Without You: Long-Term Frequency and Sequences of Acquisitions and Divestitures. Geisen, J., Aalbers, R., KJ McCarthy (2025). Academy of Management Proceedings 2025 (1), 15338

The main objective of the FINDER Project, instilled by Europe’s Digital Future Outlook, is to improve the collaborative, digitalization-driven business ecosystems between incumbent and high-tech start-ups, as drivers of Europe’s future innovation.

Europe’s Digital Future Outlook[1] urgently calls for smart, sustainable, and inclusive growth, aspiring to secure competitiveness in Europe through innovation. To reach these objectives, there is a European agenda seeking to secure competitiveness for European companies and citizens[2]. The ambition for digitally driven innovation implies a need for new business ecosystems, in which institutions, large corporations, SMEs and individuals in society will be interconnected by means of digitalization, in unprecedented ways. These innovative, yet complex, inter- organizational networks, made up of both industry incumbent and high-tech start-ups, will hopefully serve as prominent engines for future innovation within Europe’s business landscape. Many emerging digital technologies promise to have a transformational and disruptive effect on business and society at large. The benefits of new digital technology, however, are not always easy to reap, both for grassroots-emerging parties, lacking the network to get traction on their next new bright idea, but also for incumbents, that is, established players that may lack the sensitivity for the newest and latest. As a result, our broader society may miss out, as entrepreneurial potential remains untapped, and knowledge is unevenly distributed across parties.

Over the past four years the FINDER project has worked to advance scientific knowledge regarding the management of innovation, in the context of the emergent digital landscape. This has rendered working papers, several case studies on the startup-incumbent interface in the fintech domain, and last but not least, the professional and academic training of 4 early stage researchers (ESRSs) tat each are well on their way to a phd in management in the upcoming year(s). The below provides for some reflections by some of key stakeholders in this process, to whom the FINDER project team is highly grateful for their enthusiasm, coaching, sponsorship and persisting involvement over these years:

“During the last four (or so) years, we worked with the PhDs on the different deliverables that were agreed upon with our funding partner, the EU Horizon 2020 program. On top of those, the lively discussions in the group often led to additional blogs, papers, presentations and the likes thereof. It is with joy, and even some pride, we’d like to share some highlights from these with you here.

During March of 2021, Atos hosted “Inclusive Digital Innovation in Financial Services and Insurance”. During this full-week event, we produced a daily webinar in which we highlighted key topics within this very important topic for banks and insurers: how to organize innovation within an ecosystem of banks, Fintechs, authorities and customers. Among the esteemed speakers, we welcomed Josemaria Sota (IESE Business School), Hubert Tardieu (GAIA-X), Nikhil Chouguley (Deutsche Bank), Remco Veenenberg (Fintech authority) and Jeremy Abiteboul (DreamQuark). Complemented with key experts from Atos and Radboud University, the webinars drew lively discussions from the various attendees from universities, Atos, our clients and partners, and various industry bodies.

After a lively discussion in one of Radboud’s classrooms, James and Ivo decided to write a paper about their respective views on the dominance within Fintech innovation ecosystems. With the help of George Dermowidjodo, a highly experienced and well-respected banking strategy consultant, they created a paper that focusses on the dynamics between all the participants in collaborative innovation. The resulting opinion paper “Ecosystem dynamics: Understanding dominance and centrality in innovative ecosystems”, explores the collaborative innovation from the viewpoints of (incumbent) banks, Fintechs, ecosystem orchestrators and academia. The paper was peer-reviewed by the Atos Scientific Community and published on atos.net in October 2022, finding its way in the hands of hundreds of readers.

The final highlight we wish to recall are the two strategy days we organized during the closing months of the FINDER project. Atos hosted two full-day seminars on business innovation strategy and policy respectively, during the SMS London 2022 conference. During both seminars, we welcomed key leaders from both the academic and business world in our headquarters in London, where insightful presentations and passionate discussions were held to the benefit of a packed crowd. We remember vividly the great presentations by George Miller (Atos), Prof. Robert Hoskisson (Rice University), and Mario Schijven (University of Illinois) who shared their insights in behavioral bias in the topic of the first day: “Behavioral Biases and Corporate Transformation Strategies”. During the second day, the policy day on Fintech ecosystems, we distinctly remember Charleen Sparks (Lloyds Bank), who shared her experiences in orchestrating the Lloyds Bank Fintech sandbox.

For us, these highlights are obvious signs that combining academic brainpower with business acumen is a great way to elevate innovation to a new level. Another feather in the cap of the FINDER project and yet another reason to thank Rick Albers and Remco Neuteboom for their vision and hard work to bring us all together. We thank you very, very much for giving us the opportunity to be directly involved in the Finder program and equally thank Radboud University and Atos for hosting this great research program. Thanks also to Dan Cohen and Prof. Hans van Kranenburg for sponsoring us. Final thanks -and congratulations- go to James Ellis, Ami Wang, Jonas Röttger and Jonas Geisen. Working with you has been a great experience and a lot of fun. We hope, and fully expect, that we will meet again in this dynamic world of financial services & technology.

Lead the way and keep on rocking, fab four.”

Ivo Luijendijk and Frederik Kerling

Ivo Luijendijk, Atos Group Industry Director Data Analytics and Emerging Technologies – Global Financial Services and member of the Scientific Community. After 15 years experience as a banking consulting, Ivo now drives business reinvention for the Atos global financial services clients.

Frederik Kerling – Head of Fintech and Quantum industry Director – Global Financial Services and member of the Scientific Community. Frederik is specialized in bridging the gap between complicated technologies and realistic commercially viable business outcomes, and is currently heading the Fintech Engagement program with Remco Neuteboom.

[1] Foster, C. & Heeks, R.B. (2013). Conceptualizing inclusive innovation: modifying systems of innovation frameworks to understand diffusion of new technology to low-income consumers, European Journal of Development Research, 25(3), 333-355.

[1] European Commission, (2014). Europe’s Growth Strategy. Luxemburg, European Union.

I am starting off 2023 with a new project. Step by step last year’s projects come closer to version 1.0, gold status. After the realization of the joint Gaia-X whitepaper with TQ folks (see here) I’m happy to announce to be close to completing the teaching case to be published by Edward Elgar Publishing Ltd. And finally, the first working paper (at the same time being the first dissertation chapter) has been submitted for this year’s conferences. Fingers crossed. With further dissemination comes more iterations to arrive at a well-rounded paper, step by step.

And most of this from Frankfurt am Main for a large part of the year. There I was kindly “adopted” by TechQuartier for my secondment abroad Radboud’s campus in Nijmegen. Besides the academic “ivory tower”, a bit of “boots-to-the-ground” business life. In the TQ workspace, I had the pleasure of meeting fascinating people who worked either at TQ or at one of the start-ups based there. This environment helped me gain various insights relevant to my work. On the one hand, being physically present at TQ enabled me to co-author the ecosystem white paper and facilitated progress on the teaching case. On the other hand, I was sitting directly among all these different entrepreneurs gaining further insights into the development of high technology (in high technology industries). From small chats to more in-depth discussions, I was able to gain glimpses of the entrepreneurs’ work, their mindset and the way they develop (new) business models to take advantage of the opportunities created by technological developments.

Overall, I appreciate this enjoyable experience and am grateful for the open and warm welcome I received.

Here we come. Or at least that summarizes the ambition of various of the FINDER ESRs as various of them submitted to this years prime management conference to be held in Boston. Where last year showcased work in progress by Jonas Roettger (see image for the track partaken), this year offer a whole new round of working papers to be trial tested in peer review for participation.

One of the topics Ami Wang has been working on recently with such Boston ambition is THE INTERPLAY OF COOPERATION AND COMPETITION IN VENTURE CAPITAL SYNDICATION ON START-UP ACQUISITION EXIT. Drawing on embeddedness theory, her work explores the role of Venture Capitalists’ prior competitive and collaborative relationships on their start-up’s exit strategies. Evidently a relevant topic when it comes to fostering for collaborative innovation, such as the FINDER ambition is – targeting the Fintech domain. Embedded in the broader literature on Venture Capital syndication, the argument goes that VC partners’ prior cooperation and competition experience affects the success of their start-up’s acquisition exit.

In parallel work on managerial bias in strategic decision making and work on corporate divestitures has been put to the AOM test – so let’s soon find out how things land in the international academic community. Updates to follow as the work gets presented in period to come.

Cooperation between fintechs and incumbent financial institutions has become a main – if not the default – innovation strategy for the financial services industry. Pushed by developments in technology (data, digital), society (rise of the digital native generations) and regulations (PSD2/Open Finance, GDPR/data and privacy protection), banks and insurers needed to rethink the way they handle their client expectations, their workforce and the data they have available. As a result, innovation in isolation is hardly a viable model any longer, yet working with partners causes challenges of its own regarding information access, business model alignment and the general direction of the change in question. In fact, the central question behind these challenges emerges to be: What are the ecosystem dynamics, in terms of dominance and centrality?

This paper coauthored by James Ellis and Ivo Luyendijk – both FINDER tribe – explores this question in three viewpoints, related to three strategies to follow for inclusive innovation in business ecosystems. A read through provides for further understanding of the notions of ecosystem dominance and centrality in -fintech infused- innovative ecosystems.

With the start of the new year, it is also time to look back at 2022. The FINDER project has successfully concluded the past year with progression. This progression mirrors in the organized FINDER events (see here and here), conference attendance (see here and here), the completion of whitepapers (see here and here), and the first FINDER publications (see here and here). From these successful experiences, our ESRs have learned lessons that further facilitate their work along their trajectories. FINDER further joined in on the Marie Skłodowska-Curie Actions (MSCA) European industrial doctorates (EID) Cluster Event to learn from external experience as well. Conducted by the European Research Agency, the event took place in 10. November 2022 focusing on one of European Industrial Doctorate’s strong points: the interconnection of academic and non-academic practice.

This cluster event kicked off with an overview session detailing the landscape: 1,035 projects involving 12,000 ESRS are currently funded with around €3.42 billion to foster international collaboration in MSCA in Horizon Europe. The core of the event was formed by six parallel workshops where current researchers and project managers discussed and exchanged information on (i) achieving excellence in research and innovation, as well as (ii) increasing career opportunities for early-stage researchers. The six topics covered all the aspects of EID projects, specifically: Joint procedures; Administration; Mobility – Secondments – Training; Policy Workshops; Industry and business participation; Project practicalities. Hence, not only a researchers’ core activity was discussed but also valorization, international and business experience, and how to facilitate these through administration. This holistic approach allowed tracking if the Horizon projects succeeded in their aim: to enhance doctoral candidates with better career opportunities by providing them with skills formed through their experience from both academia and industry business.

In total, this event was a fitting occasion to share experiences, hurdles, and best practices across project participants of active MSCA as well as policy officers of European institutions. As such, it allowed sharing FINDER experience as well as learning from others’ experiences. Ultimately, we expect that all these learnings will feed into the ESRs pipeline leading to further FINDER successes.

Well, that’s easy: a realistic teaching case that blends various stakeholder perspectives on how to grow the business as a fintech as well as an incumbent (the status-quo). Add to that an author team consisting of various early stage researchers from the FINDER crew, several seasoned business executives and add to that two more academics and you have what SAGE publishing lists as:

To Build, Buy, or Ally: Envisioning Growth Amidst the Fintech Revolution

“Case backdrop in a nutshell: Atos is a publicly listed French multinational information technology services and business consultancy company which has experienced static growth in its stocks since its initial public offering (IPO) in 1995. However, since the heyday of 2017 when the stock peaked (ca. EUR 100 per share) the market price has dropped and stabilized at around 30% of its all-time high. Having a strongly proclaimed constant growth strategy and a substantial track record of inorganic growth undertakings, Atos currently finds itself in a situation of high expectations and high financial pressure. This was especially true given its FY19 debt of EUR 1.7 billion. How does one grow a business when there are so many options: to grow, to build, or simply to buy your way into the fintech future. What works when and why? And how about economic setback as major disruptor to some of these decisions? Check out the case and find out more. To build, buy, or ally now becomes a fundamental question for the stakeholders involved, as strategic recalibration is on the horizon.”

Congratulation to the team on bringing this case to an international audience of bachelor and master level business case students interested in better understanding the current fintech revolution.

Imagine a pond in a forest: mosquitoes lay eggs in the water; some are eaten by tadpoles; the frogs they grow into are hunted by foxes, which in turn are the mosquitoes’ prey, etc. Each have critical interdependencies; yet, which is the dominant organism? What even is dominance, anyway?

In an opinion paper that Ivo Luijendijk and S. James Ellis wrote for Atos and the FINDER Project, they grapple with these questions in innovation ecosystems contexts, where they argue that the same complexity exists. In this setting, though, it’s more than just a thought experiment: real strategic decisions can be made to achieve, exert, recover, and lose dominance; this, in turn, can make or break a business’ short-, medium-, and long-term viability and that of its interdependent partners.

You can read the opinion and summary strategic insights here; feel free to share your thoughts via LinkedIn or get in touch.

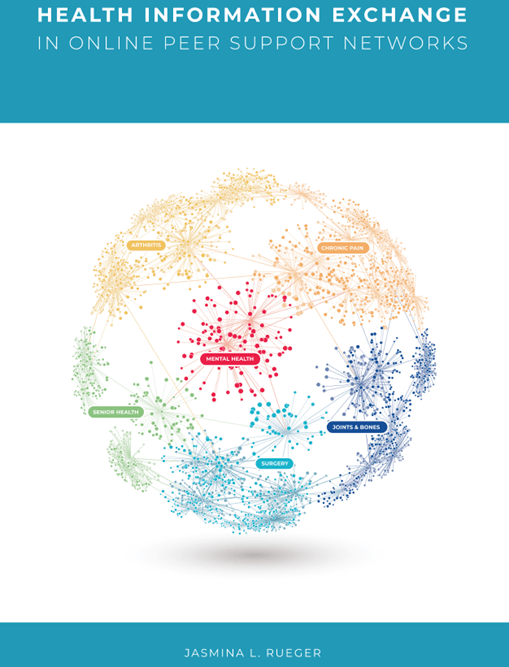

Taking part in the FINDER Amstelveen event several years ago, and recently conversing with the FINDER crowd at the SMS London, Mrs Jasmina Rueger lead by example last week by successfully defending her PhD dissertation at Wageningen University.

Focused on Health Information Exchange in Online Peer Support Networks, she addressed some governance aspects of networks that hold close resemblance to the governance of innovation networks at large also. Jasmina shared amongst others various insights into how patients discuss their health conditions and concerns online and seek support from other patients who might experience similar issues. In doing so, she suggested helpful implications that contribute to a better academic and professional understanding of the role online health communities play in helping patients access health information online and find support among their peers.

Some of the interesting aspects addressed during the defense with linkeage to network governance were:

How can researchers collect and analyse social network data from online communities to better understand relationships and information exchange in peer support networks?

To what extent does the advice sought and provided by peers online influence the emotional state of people, and in particular their negative emotions such as anxiety and depression?

How is peer advice appreciated differently depending on the level of similarity in the knowledge and experiences of the adviser and advisee?

Exploring Tweets about covid-19 vaccination preferences as an example of a polarised debate, how do emotions and information being exchanged online influence the diffusion of pro- and anti-vaccine sentiment on Twitter?

Members of the reading committee included:

Prof. Dr D.S. Moore Jr., Wageningen University & Research

Prof. Dr A. Boonstra, University of Groningen

Prof. Dr C.T.B. Ahaus, Erasmus School of Health Policy & Management, Rotterdam

Prof. Dr J. Pfeffer, Technical University of Munich, Germany

Most interesting work, proud to have served as your co-promotor over the past few years together with Prof. Wilfred Dolfsma of WUR. Congratulations Dr Rueger! Your achievement has certainly been inspirational to the team over here.