Rick Aalbers (Radboud University, IMR) and Koen Heimeriks (Warwick Business School), have put together the SMS Extension Conference “Behavioral Biases and Corporate Transformation Strategies”. The event is open to seasoned practitioners and academics, as well as early PhD stage researchers as a foundation for future collaboration.

It promises to be an exciting full day program that touches upon various central aspects of corporate transformation and its underlying behavioral biases as strategy gets drafted and executed under transformative intent.

Technological disruption, digital innovations, and societal changes have pushed corporate transformation to top executive agendas. While this propels the importance of a firm’s propensity and ability to divest, acquire, and collaborate, behavioral biases can significantly implicate the decision making and implementation of these strategic tasks. This Extension highlights new insights and theories that shed light on how behavioral bias affect strategic decision making.

Under this theme we present the following inspiring set of speakers and discussants:

Phil Dunny, Managing Partner Ronald Berger London

Robert Hoskisson, George R. Brown Professor Emeritus of Management, Rice University

Francesco Castellaneta, Professor of Strategy and Entrepreneurship, SKEMA

Emilie R. Feldman, Michael L. Tarnopol Professor of Management, University of Pennsylvania

Chris Vialle, Partner Monitor Deloitte

Mark DesJardine, The Pennsylvania State University

Gerry McNamara, the McConnell Professor of Management, Michigan State University

Himanshu Vyas, Chief Strategy Officer, Atos, UK

Mario Schijven, Assistant Professor of Business Administration, University of Illinois

Based on this speaker set we offer a full day program, that revolves around three distinct, yet intertwined themes across several sessions on behavioral biases in strategic tasks, with the intent to open up dialogue on the intersection between academia and practice.

Each of the sessions will showcase various angles on the initiation of and the responses to strategic tasks. Relative to the main (track) questions, a variety of panelists combining academic and practitioner backgrounds will discuss the characteristics of strategic decisions (to be) made, as well as the behavioral characteristics of management relative to those of other active stakeholders to the decision making and implementation process will be scrutinized.

At the end of the day, a social event will be hosted at one of the London Pubs to offer a great final experience to all participants.

Join us in September for this thought-provoking event that couples academia and practice on corporate strategy level. Details and registration information can be found here.

Two weeks ago the European Academy of Management community came together to host their annual conference; for the first time in person since the onset of the COVID-19 pandemic. Two years in isolation did not harm the quality of the work presented and the FINDER team was pleased to contribute to the program by delegating ESR Jonas Röttger to present a working paper on behavioral signal sets in acquisition announcements. The valuable feedback of the reviewers and the audience at EURAM will support enhancing the quality of the study further.

Gaia-X aims to build a new generation of transparent, controllable, and interoperable services that implement a common set of rules shared by hundreds of European and non-European players in the market to bolster the European sovereignty in digitalisation and the data economy.

However, can one orchestrate such an ecosystem? And if so, who should be the orchestrator and how should one go about it?

In our contribution to the Gaia-X newsletter, Luisa Kruse, Sebastian Schäfer – both from our FINDER partner TechQuartier – and I deep-dived into the project safe Financial Big Data Cluster (FBDC) to extrapolate answers for such an approach of open innovation.

We find that innovation hubs are in a prime position to take over the role of an orchestrator of a publicly funded ecosystem. To make most of the complementary, modular actors within such an ecosystem we suggest a hybrid orchestration form. Finally, it is important to mention that a successful ecosystem not only needs orchestrators but also contributors to create something new and valuable. At best, these should be innovative and have the capability to lead the ecosystem to new perspectives and products.

The complete version of our contribution is available to download below:

Together with Rick Aalbers (Radboud University, IMR) & Koen Heimeriks (Warwick Business School), we have put together an exciting full day program that touches upon various central aspects of corporate transformation and its underlying behavioral biases as strategy gets drafted and executed under transformative intent.

Technological disruption, digital innovations, and societal changes have pushed corporate transformation to top executive agendas. While this propels the importance of a firm’s propensity and ability to divest, acquire, and collaborate, behavioral biases can significantly implicate the decision making and implementation of these strategic tasks. This Extension highlights new insights and theories that shed light on how behavioral bias affect strategic decision making.

Under this theme we present the following inspiring set of speakers and discussants:

Phil Dunny, Managing Partner Ronald Berger London

Robert Hoskisson, George R. Brown Professor Emeritus of Management, Rice University

Francesco Castellaneta, Professor of Strategy and Entrepreneurship, SKEMA

Emilie R. Feldman, Michael L. Tarnopol Professor of Management, University of Pennsylvania

Chris Vialle, Partner Monitor Deloitte

Mark DesJardine, The Pennsylvania State University

Gerry McNamara, the McConnell Professor of Management, Michigan State University

Himanshu Vyas, Chief Strategy Officer, Atos, UK

Mario Schijven, Assistant Professor of Business Administration, University of Illinois

Based on this speaker set we offer a full day program, that revolves around three distinct, yet intertwined themes across several sessions on behavioral biases in strategic tasks. With the intent to open up dialogue on the intersection between academia and practice. The event is open to seasoned practitioners and academics, as well as early PhD stage researchers as a foundation for future collaboration. Each of the sessions will showcase various angles on the initiation of and the responses to strategic tasks. Relative to the main (track) questions, a variety of panelists combining academic and practitioner backgrounds will discuss the characteristics of strategic decisions (to be) made, as well as the behavioral characteristics of management relative to those of other active stakeholders to the decision making and implementation process will be scrutinized.

At the end of the day, a social event will be hosted at one of the London Pubs to offer a great final experience to all participants.

We hope you will join us in September for this thought-provoking event that couples academia and practice on corporate strategy level. Details and registration information can be found here.

After successfully defending my research proposal titled ’The influence of temporality on exogenous growth strategies – Alternative business models in digital ecosystems’ in October 2021 I have been putting my focus on the first chapter of my dissertation.

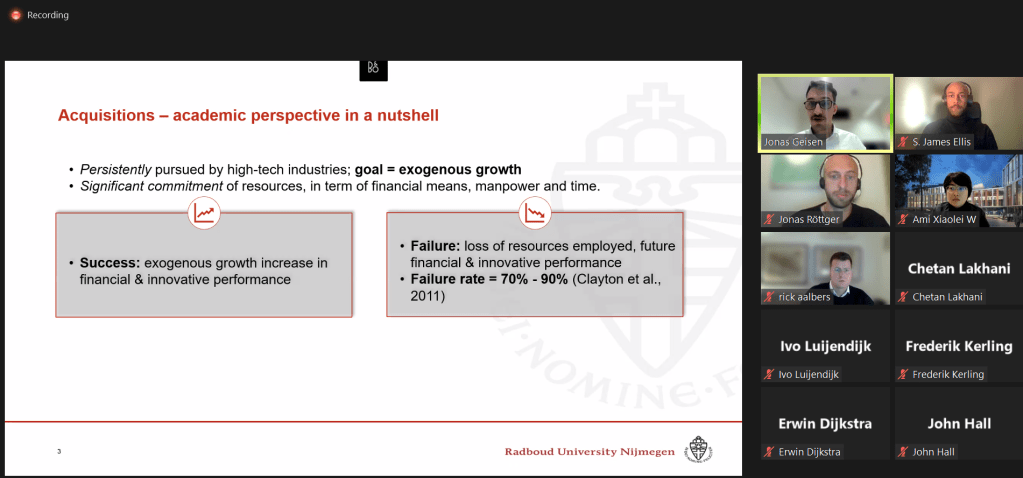

Since then, under the title ’Dancing to the Rhythm: the Dynamics of Acquisition Motive on Acquisition Programmes’, I have been working on my first paper with Dr. Rick Aalbers (Radboud University) and Dr. Killian J. McCarthy (Rijksuniversiteit Groningen), both from the Centre for Strategic Organizational Restructuring. After 5 months of theoretical build-up, data gathering, learning to work with the statistical software R to crunch numbers, and crunching said numbers I thus was more than happy to present our paper under the umbrella of the strategy underlying corporate development. Zooming in one specific aspect of corporate development, we investigate firms’ acquisitive behaviour, a mean to pair firms of selected high-tech industries with not only incumbent players but also fintechs.

Acquisitions keep being a major governance mode for high-tech organizations despite being both risky (measured by the high rate of failure) as well as resource-consuming over longer periods. However, if successful this strategic activity is a bedrock to evolve the firm’s portfolio or even business model while shaking up digital ecosystems. Therefore, the effect on repetitive acquirers’ financial performance ensures survivability in their fast-paced industries. As our paper unravels the underlying dynamics of serial acquisition programmes it provides a crucial new perspective for strategic management scholarship’s understanding.

Given this thematic embeddedness, it was more than fitting to invite the Strategy Department of the Nijmegen School of Management as well as the Hotspot Innovation and Entrepreneurship in Business Ecosystems of Radboud University as the audience to premiere our work. Jointly, we deep-dived into the paper, investigating the theoretical framework, the concepts, and their interrelated mechanisms as well as their methodological operationalization for the analysis. Finishing up with our results, our work was discussed with a positive prospect as well as focused feedback making the session both a pleasure as well as a helpful perspective on how to further flesh out our piece. We thank all participants who made this lively session a fruitful next step in our development.

As FINDER sets out to Foster Innovation Networks in a Digital Era in a European, this Industrial Doctorate partnership of 4 years between Radboud University and Atos has been on its way now for close to 3 years already. Time thus to report on some of the progression made to date. This portal has outlined various of these initiatives over the past years, including the hosting of various startup initiatives, including a startup weekend with participants from 3 continents and various technology domains, doctoral workshops, student oriented case study initiatives and – last but not least – collaborative research being presented at sone of the major international conference in the field of management. These academic venues include such as the Academy of Management, EGOS (European Group for Organization Studies) and EURAM (the European Academy of Management). All activities are driven by the ambition to prepare a new generation of business and entrepreneurship researchers contributing to the development of innovative ecosystems in a digital era.

On that note below a review of the progression per Early Stage Career (ESR) track:

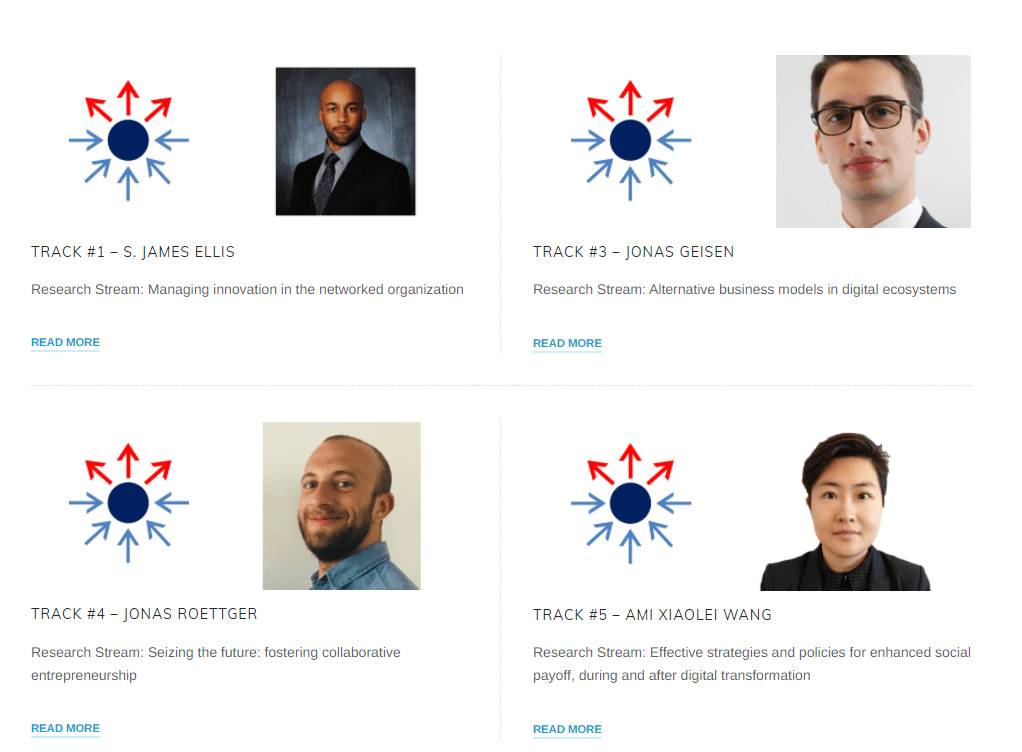

ESR Track 1’s research on collaborative innovation management addresses gaps in organizational sciences literature concerning the sociopolitical forces behind technological innovation as it occurs between firms and other firms, between firms and regulators, and between firms and society. There are no clear indications that businesses engaged in high-tech ecosystems will divert away from collaborative innovation approaches, which makes this research and the tools it produces timely and useful in elucidating the challenges that practitioners presently face and will face in the future.

ESR Track 3’s research is relatively embryonic, for the ESR only joined the project in November 2020 following a resignation. This ESR has already achieved considerable progress, focusing on how uncertainty in times of crisis triggers organizational transformation. As the world has been rocked by economic, pathologic, and climate-related disasters with no signs of slowdown in the future, understanding how companies survive and adapt to major turbulence is crucial for strategic management scholarship’s understanding.

ESR Track 4 also deals with the social forces at play in interfirm decision-making. The role of positional icons such as CEOs is significant in events such as mergers and acquisitions. This research uses novel methods to examine the signals that CEOs advertently and inadvertently cast when announcing their M&A decisions, which promises to broaden the managerial sciences’ scope on the applicability of investigative machine learning.

ESR Track 5’s focus on venture capital (VC) as a fuel for the entrepreneurship of technological innovation provides a different lens on the social aspect of interorganizational relationships. Quantitative research methods will allow this track to investigate how the VCs’ reputation interplays with their funding targets’ performance. The practical applications of this research will largely be for the parties engaged in this dialogue, but as investing overall becomes more democratized, insights therefrom promise to become more widely applicable as they age.

All ESRs completed or at least entered into their secondments, digitally and now then finally also – on site again, with Jonas Geisen embedded at TQ Frankfurt for the coming half year, as COVID restrictions are eased to a level that accommodates for such field work again.

Training

As for academic training all ESRs had their research proposals accepted by the Radboud Scientific Advisory Committee. All ESRs also partook in the FINDER-led Research Excellence Workshop in February 2020 as well as the Strategic Management Society Berkeley Doctoral Workshop held virtually in November 2020. Currently each candidate is wrapping up – or has already rounded up – the business side of the training .

ESR Track 1 has completed 24 ECTS of doctoral training, ESR Track 3 has not yet completed ECTS, but is currently taking training that will allow for 9 ECTS of doctoral training, ESR Track 4 has completed 17 ECTS of doctoral training, and ESR Track 5 has completed 26 ECTS of doctoral training portfolio on offer via ATOS, experiencing the very same training opportunity as open to the broader ATOS workforce.

In the course of the research methodologically outlined as part of this ITN proposal, some outputs have already come to fruition including manuscript submissions and acceptances to the 2020 and 2021, European Group for Organization Studies Colloquia, 2021 Academy of Management Annual Conference, the 2021 International Process Symposium and the 2021 European Academy of Management Annual Conference., and most recently also the 2022 EURAM conference as first 2022 onsite event to take place in Switzerland this year. With papers targeted at the 2022 AOM, SMS and also the local paper workshop venues (national university level) research exposure is certainnly consolidated on by the ESRs, a job well done!

example of a conference that featured FINDER inputs

Then in terms of expected potential impact:

As the FINDER research scope spans industries and job functions, it requires candidates to synthesize complex information and to approach problems nimbly in a manner that can be transferred to both academics and practitioners. FINDER’s integrated curriculum prepares the ESR’s to drive change at the vanguard of business and technology by challenging them to consider multiple perspectives and to create innovative solutions to problems in such a way that they are not only profitable to business but also relevant and responsible towards society at large.

As each of the Marie Curie FINDER PhD Fellows investigates an aspect of innovative collaborative arrangement amongst organizations –such the various configurations possible among grassroots, incumbents and the wider society as they inclusively explore digital technology for new product or market development, impact is diverse also.

the main ambitions are summarized per track in the following general objectives – with associated research questions, as has become evident over the past years of reporting on each of those on this portal:

Managing innovation in the networked organisation RQ: How do digital technologies influence systems, practices and processes for the effective management of innovation within and across organisations?

Seizing the future: fostering collaborative entrepreneurship RQ: What are the characteristics of alternative business models in digital ecosystems? Which factors facilitate their development?

Alternative business models in digital ecosystems RQ: What are the internal and external contingencies that explain the diverse organisational arrangements seen in new ventures? How does the internal organisation of entrepreneurial ventures interact with governance, ownership, industry and geography?

Effective strategies and policies for enhanced social payoff, during and after digital transformation RQ: What are the roles, challenges and opportunities for incumbent firms and newcomers for a sustainable transition to digital technologies? How can organisations overcome struggles over the meaning of sustainability, within and across organisational fields, as the digital ecosystem unfolds?

In the period to come you can expect further policy reflections on each of those questions posted by the ESRs. So stay tuned. Promising future outcomes in this regard per track are:

Track 1 continued ethnographic research will provide insights that non-FINDER academics have commented on as important to the field, with a closeness to data not often seen in this discipline. Insights promise a close fit to both policymakers and practitioners, as ongoing collaboration in the direct Fintech realm is being reflected on from various theoretical angles. In depth case work that makes it into policy advice.

Track 3 has recently consolidated on empirical evidence that unpacks some of the dynamics that back high tech oriented serial acquisitions. With M&A making up for a major governance mode to pair fintech startups with incumbent players, this project is particularly fitting to the FINDER ambition to review the various characteristics of alternative business models in digital ecosystems. For instance, and despite the reoccurrence of failure, high-tech organizations are persistent in their pursuit of their next acquisition, committing significant resources to this strategic activity in the process. In this study, and drawing on organization learning theory, novel theoretical arguments are developed to connect a firm’s repetitive acquisition portfolio decisions to its short and long term market performance.

Track 4, particular to the employed methodology, is amassing a dataset of CEO M&A announcements which will provide a baseline for further analysis in this track for future academic and white paper submissions. Policy advice will advocate the need to pay attention to behavioral effects when orchestrating collaboration – as via mergers or acquisitions – in the technology domain.

Track 5 experienced pandemic-specific delays that necessitated a shift in data collection; nonetheless, this track currently consolidates on rich data on the collaboration between Venture Capitalists, startups and incumbents as they try to team up towards a successful tech – as well as non tech oriented service offering. What configuration works best? What is the role of partner diversity, timing and innovation at large as these mini-consortia team up in pursuit of the next IPO or acquisition? Policy advice will be backed by quantitative evidence to reflect on these questions in the near future.

All tracks will reflect on the societally responsible aspects of their advice, thus considering employment next to profit, long term societal aspirations next to short term financial gain, applying a multiple stakeholder approach to their conclusions.

Scenario: your large, multinational firm has just completed a costly acquisition, yet one that promises to increase your global revenues by a considerable margin. Yet, your share prices keep steadily declining, and your investors are starting to show negative sentiment towards your stock. If you don’t act quickly with some sort of whizbang, strategic solution, lucrative opportunities elsewhere in the space might decay your investor base, triggering a sell-off and catastrophes of unknown number and magnitude thereafter. What do you do?

Luckily – or hopefully – you’re not actually in that scenario. Someone probably is, somewhere in the world, and we’d love to help. But in the meantime, we here at the FINDER project are more concerned with building a corps of strategists who can not only solve these problems in situ, but see them coming from a mile/kilometer away and make prescient moves to help their firms avoid these rough waters.

Recently, SAGE Business Cases, a premier-if-not-the-premiere business and teaching case publisher, accepted a teaching case for publication that the FINDER team submitted last year. Typically, academic researchers dedicate most or all of their research efforts to publishing their work in strictly academic journals – in the scope of FINDER, this might mean theoretical work intended to (slightly) shift a discipline’s collective way of thinking. A tall order, to say the least, and this shows in the many years that it often takes for such a work to go from first draft to accepted publication. However, this is not universal law: an exemplary exception is the recent PLOS ONE article that Dr. Rick Aalbers, Jonas Röttger, and colleagues published which examines market reactions to certain strategic orientations in the wakes of firm acquisitions.

With teaching cases, though, the motivation is different. Rather than shifting academic thought, these articles are meant to provide educators with tools to build academic thought. Thinking in the scope of business schools and business cases: corporate strategy is concerned with teaching students to examine complex matrices of phenomena from a central headquarters’ point of view, prescribe solutions for the firm, and measure the effects of those decisions and deployments to achieve certain prescriptions. Short form: consulting by any other name. In all seriousness, though, these skills are useful for careers well beyond consulting. Strategic thinking of the kind I just described finds a home in political sciences, small business founding, tech development, and many more arenas.

It is our hope that the teaching case will find use in classrooms around the world and wherever educators and students alike are concerned with ideating strategic solutions to organizational problems. The case, as well as many others, can be found at https://sk.sagepub.com/cases/discipline. If you’d like to use the case, feel free to go through the above link or to contact us through this website or LinkedIn.

– S. James Ellis

Please cite the case as:

Aalbers, R., Ellis, S., Khanagha, S., Luijendijk, I., Neuteboom, R., & Röttger, J., (2022). To build, buy, or ally: Envisioning growth amidst the fintech revolution. In SAGE Business Cases. SAGE Publications, Ltd., https://dx.doi.org/10.4135/9781529793840

We are proud to announce that members of the FINDER project team reached the semi-finals in the Mercator Innovation Competition with their idea of improving Fintech scouting for banks.

Mercator Launch is a pre-incubator for early phase entrepreneurship. The Mercator Innovation Competition comprises of an evaluation committee installed with representatives of Radboud Innovation / Valorisation Radboudumc.

This evaluation committee will select 6 finalists, who get to pitch their idea in front of an independent jury and their peers. The winner will receive a cash prize of €10.000 to spend on further development of their innovation, business coaching, and a free working space at Mercator Launch for one year.

We are very proud to announce that PLOS ONE published a research article by members of the FINDER team: Rick Aalbers and Jonas Röttger, who joined forces with Killian McCarthy and Menno Huisman, resulting into:

“Moving motives: How past and present strategy influence the market”

In the article the authors discuss how research often only considers the performance of a single acquisition, or the effects of a single acquisition on the performance of the acquiring firm, showing that acquisition motive matters. However, firms often make multiple acquisitions and research recognizes that firms must both explore and exploit to sustain their competitiveness. There is evidence too to suggest that firms use some acquisitions to explore and others to exploit.

This raises a number of interesting questions. For example, do investors take the ’portfolio’ of acquisitions into account when reacting to an announcement of an acquisition? Does the market react to the switch in strategy from exploration to exploitation? And if it does, does the market prefer a switch to exploration or exploitation?

Read the full article in which Rick, Kilian, Jonas and Menno investigate the market’s reactions to serial acquirers that switch strategy here.

In the FINDER project, with a broader scope, we investigate how the continuously increasing pace of digitalization shapes the collaborative innovation of firms. Such innovative trajectories do not necessarily pan out in a linear fashion. In fact, they can even hold the potential to induce strategic reorganization of firms’ organizational form (The Centre for Organization Restructuring hosted by Radbouds’ Institute for Management Research bundles expertise on this field). Such change can have different antecedents either originating in an approach of long-range planning or a firm’s threat of survival. In all cases, however, one needs to acknowledge that such a strategic reorganization holds advanced interdependencies to their collaborative networks.

FINDER, as a project by Radboud University & Atos, therefore hosted a two-day symposium to examine the influence of Atos’ strategic reorganization of its vertical Financial Services & Insurances (FS&I) on its innovative collaboration network.

In order to make full use of the intersection between academia and practice, the symposium was divided into two days to provide the necessary space to explore both perspectives. The first day provided various intra-organizational angles onto Atos transformation to transmit a holistic picture. Connecting the inputs of the first day with the ESRs focal points of research on the second day delivered new perspectives rooted in research on said transformation.

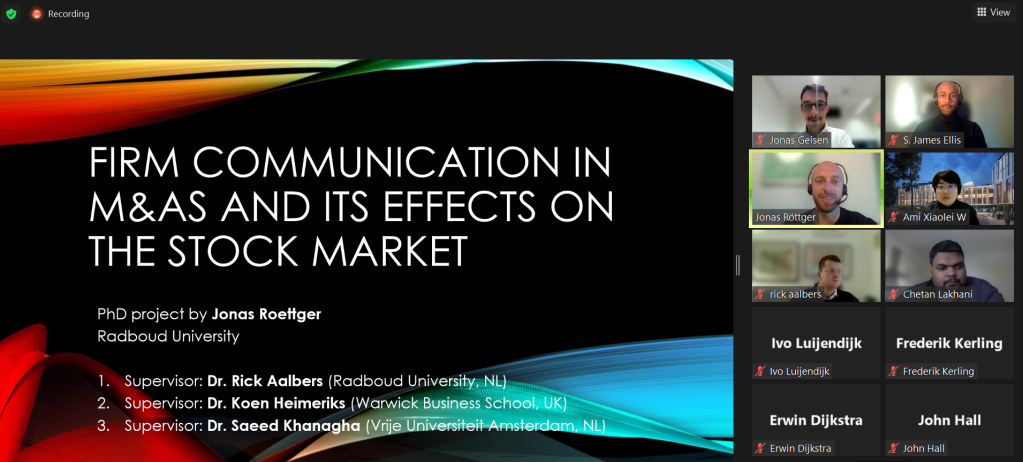

Together with members of the Atos Scientific Community, the Atos Scaler program, and the FS&I leadership team we fruitfully discussed how digital technologies necessitate an intra- and entrepreneurial handling of digital technologies. The focus was on the combination of large (corporates) and small (FinTechs) organizations in the Financial Services Industry and upper management’s role as policy-makers to facilitate new ventures. More specifically there were four different topics discussed on the second day:

Jonas Röttger: Firms communication in M&As and its effect on the stock market

Jonas Geisen: Dancing to the rhythm: the dynamics of acquisition motive on serial acquisition

S. James Ellis: Ecosystem dominance – three approaches to emerge on top

Ami X. Wang: Incumbents and Entrepreneurial ventures In The Digital Era

Highlighted by the interest of the participants in the insights it becomes apparent that there is a demand for diffusion and direct application of scientific knowledge. This symposium and FINDER, due to its unique feature of intersecting academia and industry, serve this purpose through research that provides meaningful insights to understand and foster innovation for and applicable by practitioners. We are happy to share that this symposium, with its collaborative format and fruitful discussions with Atos, successfully delivered on FINDERs purpose of an ambilateral diffusion of knowledge achieving an incremental impact for both academia and practice. This becomes more visible in its outcome as the practitioners provided the ESRs with hands-on input for their research while the ESRs presented new perspectives derived from research for Atos practitioners.