On Wednesday, March 17th, S. James Ellis gave a talk concerning ecosystem dominance at the weeklong Inclusive Digital Innovation event hosted by Atos. This discussion comes in the wake of a white paper currently in development centered around the same topic.

The paper views dominance through three different lenses in order to prescribe what incumbent and startups should focus on to gain a dominant edge in digital, data-driven ecosystems. “Dominance,” in this sense, is given a fair amount of room for interpretation, but it hinges on the idea that in an ecosystem where a business’ stakeholders seek sustainable revenue going forward, there exists the possibility to adapt to ecosystem changes while simultaneously gaining some measure of influence over how a company’s peers in an ecosystem engage with each other. This all centers on a core tenet of ecosystems being the variety of interactions between members.

Customer Access

The first argument asserts that customer access – distinct from customer engagements – is a path to focus on when seeking a dominant position in ecosystems. While many companies do indeed prioritize interaction with their customers as a general objective, this point of view suggests that building the material or conceptual infrastructure to own engagement with the customer is key to gaining a dominant advantage. This could be actualized, for instance, through building “vessel offerings,” where the focal company bundles its own offerings alongside complementary companies’ offerings. The example James gave was that of Internet companies that bundle television companies’ offerings in with their own services, thereby owning access to the Internet and television customer. As the customer, in this perspective, is assumed to be the leading force in ecosystem innovation, this begets an advantage in seizing customer-led innovation opportunities – and thus, a sense of dominance concerning this.

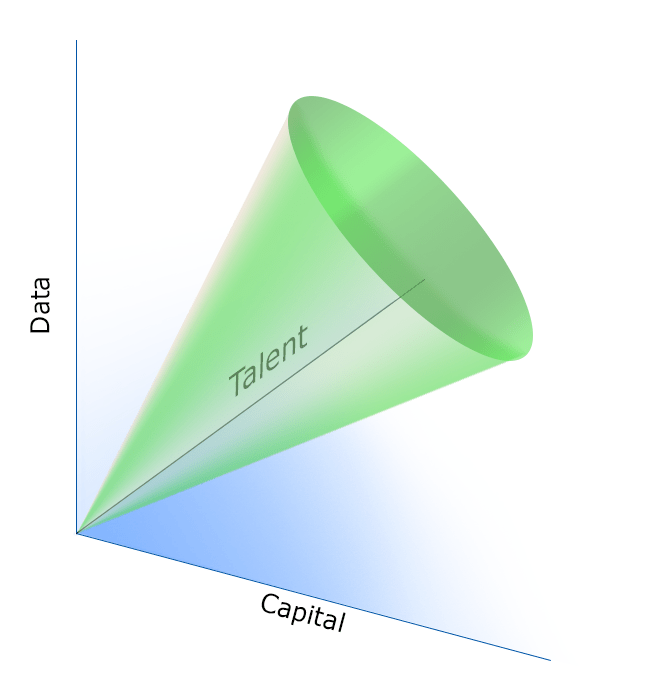

Resources

Similar to hallmark resource-based approaches, this viewpoint asserts that access to key resources is the key to finding a dominant position in ecosystems. However and somewhat particular to data-driven ecosystems, these key resources are interrelated proportionately. That is, a company must achieve an interlinked balance of capital, talent, and data in order to most effectively advance its position in its ecosystem. This viewpoint further posits that an overage of any of these resources without a correlated gain in the other two will result in an inefficient operating position, which could slow the company down enough to jeopardize its dominant advantage.

Ecosystem Centrality

The final viewpoint asserts that a company that systematically pursues the most ecosystem connections, thus centralizing itself among participants, stands to gain a dominant edge among peers. By establishing material linkages with other companies, such as supply chain redundancies, formalized partnerships in joint offerings, and the like, this central and centralizing company begins to insulate itself from the inevitable failures and disruptions that occur in ecosystems, and especially those experiencing the turbulence of broadscale innovation.

The white paper will be available through Atos’ Thought Leadership publications later this year.

Other sessions in the event were given on de-risking corporate startups by Josemaria Siota, GAIA-X by Hubert Tardieu, life-fulfillment services as can be offered by retail banks by Eddy Claessens, and enabling next generation customer insights and interactions through explainable AI by Jeremie Abiteboul.