I am starting off 2023 with a new project. Step by step last year’s projects come closer to version 1.0, gold status. After the realization of the joint Gaia-X whitepaper with TQ folks (see here) I’m happy to announce to be close to completing the teaching case to be published by Edward Elgar Publishing Ltd. And finally, the first working paper (at the same time being the first dissertation chapter) has been submitted for this year’s conferences. Fingers crossed. With further dissemination comes more iterations to arrive at a well-rounded paper, step by step.

And most of this from Frankfurt am Main for a large part of the year. There I was kindly “adopted” by TechQuartier for my secondment abroad Radboud’s campus in Nijmegen. Besides the academic “ivory tower”, a bit of “boots-to-the-ground” business life. In the TQ workspace, I had the pleasure of meeting fascinating people who worked either at TQ or at one of the start-ups based there. This environment helped me gain various insights relevant to my work. On the one hand, being physically present at TQ enabled me to co-author the ecosystem white paper and facilitated progress on the teaching case. On the other hand, I was sitting directly among all these different entrepreneurs gaining further insights into the development of high technology (in high technology industries). From small chats to more in-depth discussions, I was able to gain glimpses of the entrepreneurs’ work, their mindset and the way they develop (new) business models to take advantage of the opportunities created by technological developments.

Overall, I appreciate this enjoyable experience and am grateful for the open and warm welcome I received.

With the start of the new year, it is also time to look back at 2022. The FINDER project has successfully concluded the past year with progression. This progression mirrors in the organized FINDER events (see here and here), conference attendance (see here and here), the completion of whitepapers (see here and here), and the first FINDER publications (see here and here). From these successful experiences, our ESRs have learned lessons that further facilitate their work along their trajectories. FINDER further joined in on the Marie Skłodowska-Curie Actions (MSCA) European industrial doctorates (EID) Cluster Event to learn from external experience as well. Conducted by the European Research Agency, the event took place in 10. November 2022 focusing on one of European Industrial Doctorate’s strong points: the interconnection of academic and non-academic practice.

This cluster event kicked off with an overview session detailing the landscape: 1,035 projects involving 12,000 ESRS are currently funded with around €3.42 billion to foster international collaboration in MSCA in Horizon Europe. The core of the event was formed by six parallel workshops where current researchers and project managers discussed and exchanged information on (i) achieving excellence in research and innovation, as well as (ii) increasing career opportunities for early-stage researchers. The six topics covered all the aspects of EID projects, specifically: Joint procedures; Administration; Mobility – Secondments – Training; Policy Workshops; Industry and business participation; Project practicalities. Hence, not only a researchers’ core activity was discussed but also valorization, international and business experience, and how to facilitate these through administration. This holistic approach allowed tracking if the Horizon projects succeeded in their aim: to enhance doctoral candidates with better career opportunities by providing them with skills formed through their experience from both academia and industry business.

In total, this event was a fitting occasion to share experiences, hurdles, and best practices across project participants of active MSCA as well as policy officers of European institutions. As such, it allowed sharing FINDER experience as well as learning from others’ experiences. Ultimately, we expect that all these learnings will feed into the ESRs pipeline leading to further FINDER successes.

Gaia-X aims to build a new generation of transparent, controllable, and interoperable services that implement a common set of rules shared by hundreds of European and non-European players in the market to bolster the European sovereignty in digitalisation and the data economy.

However, can one orchestrate such an ecosystem? And if so, who should be the orchestrator and how should one go about it?

In our contribution to the Gaia-X newsletter, Luisa Kruse, Sebastian Schäfer – both from our FINDER partner TechQuartier – and I deep-dived into the project safe Financial Big Data Cluster (FBDC) to extrapolate answers for such an approach of open innovation.

We find that innovation hubs are in a prime position to take over the role of an orchestrator of a publicly funded ecosystem. To make most of the complementary, modular actors within such an ecosystem we suggest a hybrid orchestration form. Finally, it is important to mention that a successful ecosystem not only needs orchestrators but also contributors to create something new and valuable. At best, these should be innovative and have the capability to lead the ecosystem to new perspectives and products.

The complete version of our contribution is available to download below:

After successfully defending my research proposal titled ’The influence of temporality on exogenous growth strategies – Alternative business models in digital ecosystems’ in October 2021 I have been putting my focus on the first chapter of my dissertation.

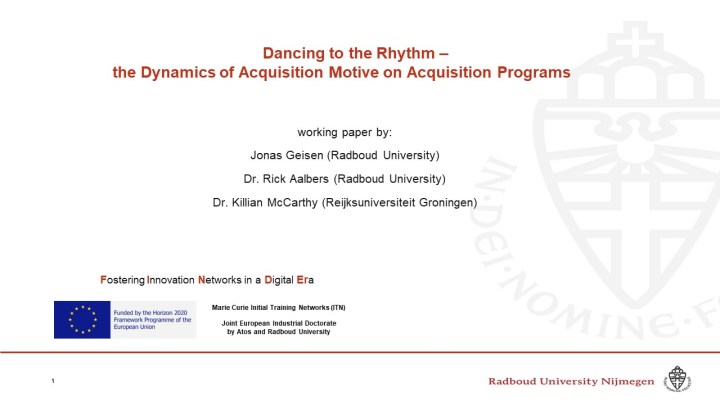

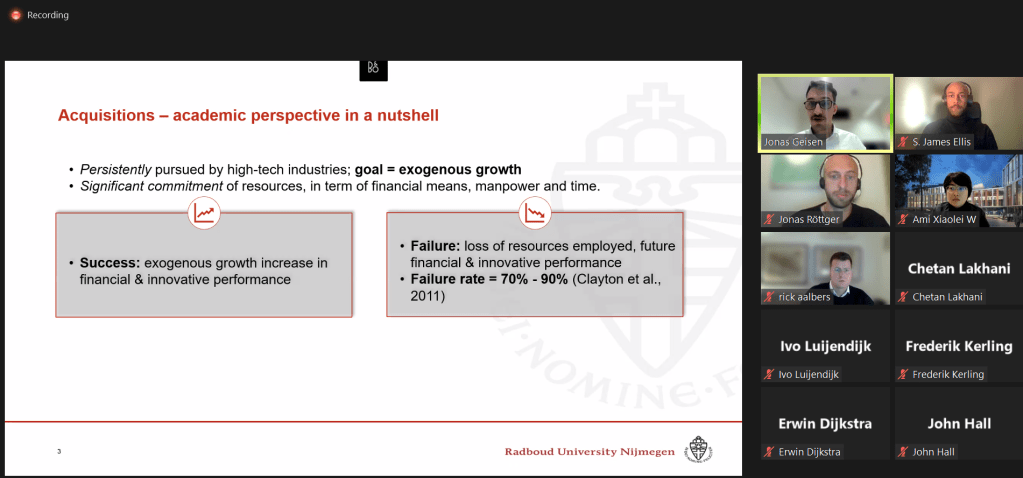

Since then, under the title ’Dancing to the Rhythm: the Dynamics of Acquisition Motive on Acquisition Programmes’, I have been working on my first paper with Dr. Rick Aalbers (Radboud University) and Dr. Killian J. McCarthy (Rijksuniversiteit Groningen), both from the Centre for Strategic Organizational Restructuring. After 5 months of theoretical build-up, data gathering, learning to work with the statistical software R to crunch numbers, and crunching said numbers I thus was more than happy to present our paper under the umbrella of the strategy underlying corporate development. Zooming in one specific aspect of corporate development, we investigate firms’ acquisitive behaviour, a mean to pair firms of selected high-tech industries with not only incumbent players but also fintechs.

Acquisitions keep being a major governance mode for high-tech organizations despite being both risky (measured by the high rate of failure) as well as resource-consuming over longer periods. However, if successful this strategic activity is a bedrock to evolve the firm’s portfolio or even business model while shaking up digital ecosystems. Therefore, the effect on repetitive acquirers’ financial performance ensures survivability in their fast-paced industries. As our paper unravels the underlying dynamics of serial acquisition programmes it provides a crucial new perspective for strategic management scholarship’s understanding.

Given this thematic embeddedness, it was more than fitting to invite the Strategy Department of the Nijmegen School of Management as well as the Hotspot Innovation and Entrepreneurship in Business Ecosystems of Radboud University as the audience to premiere our work. Jointly, we deep-dived into the paper, investigating the theoretical framework, the concepts, and their interrelated mechanisms as well as their methodological operationalization for the analysis. Finishing up with our results, our work was discussed with a positive prospect as well as focused feedback making the session both a pleasure as well as a helpful perspective on how to further flesh out our piece. We thank all participants who made this lively session a fruitful next step in our development.

In the FINDER project, with a broader scope, we investigate how the continuously increasing pace of digitalization shapes the collaborative innovation of firms. Such innovative trajectories do not necessarily pan out in a linear fashion. In fact, they can even hold the potential to induce strategic reorganization of firms’ organizational form (The Centre for Organization Restructuring hosted by Radbouds’ Institute for Management Research bundles expertise on this field). Such change can have different antecedents either originating in an approach of long-range planning or a firm’s threat of survival. In all cases, however, one needs to acknowledge that such a strategic reorganization holds advanced interdependencies to their collaborative networks.

FINDER, as a project by Radboud University & Atos, therefore hosted a two-day symposium to examine the influence of Atos’ strategic reorganization of its vertical Financial Services & Insurances (FS&I) on its innovative collaboration network.

In order to make full use of the intersection between academia and practice, the symposium was divided into two days to provide the necessary space to explore both perspectives. The first day provided various intra-organizational angles onto Atos transformation to transmit a holistic picture. Connecting the inputs of the first day with the ESRs focal points of research on the second day delivered new perspectives rooted in research on said transformation.

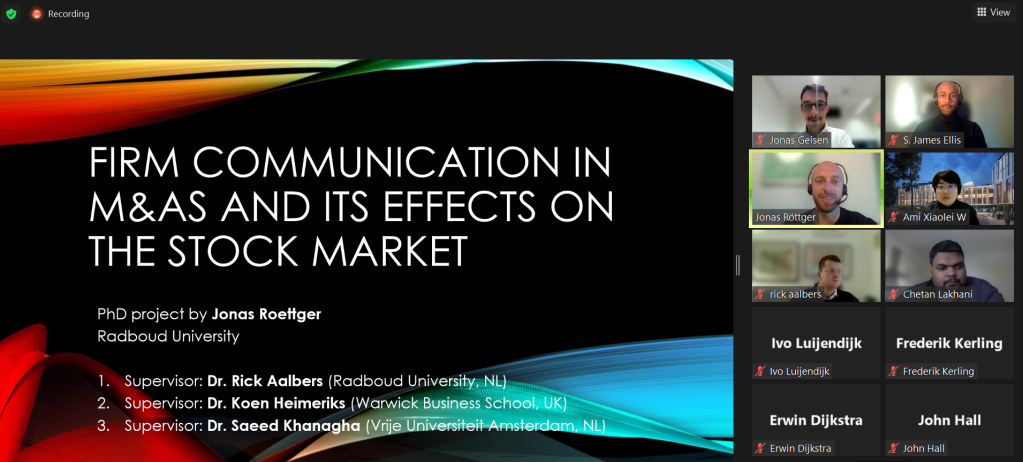

Together with members of the Atos Scientific Community, the Atos Scaler program, and the FS&I leadership team we fruitfully discussed how digital technologies necessitate an intra- and entrepreneurial handling of digital technologies. The focus was on the combination of large (corporates) and small (FinTechs) organizations in the Financial Services Industry and upper management’s role as policy-makers to facilitate new ventures. More specifically there were four different topics discussed on the second day:

Jonas Röttger: Firms communication in M&As and its effect on the stock market

Jonas Geisen: Dancing to the rhythm: the dynamics of acquisition motive on serial acquisition

S. James Ellis: Ecosystem dominance – three approaches to emerge on top

Ami X. Wang: Incumbents and Entrepreneurial ventures In The Digital Era

Highlighted by the interest of the participants in the insights it becomes apparent that there is a demand for diffusion and direct application of scientific knowledge. This symposium and FINDER, due to its unique feature of intersecting academia and industry, serve this purpose through research that provides meaningful insights to understand and foster innovation for and applicable by practitioners. We are happy to share that this symposium, with its collaborative format and fruitful discussions with Atos, successfully delivered on FINDERs purpose of an ambilateral diffusion of knowledge achieving an incremental impact for both academia and practice. This becomes more visible in its outcome as the practitioners provided the ESRs with hands-on input for their research while the ESRs presented new perspectives derived from research for Atos practitioners.

The success of the safeFBDC depends on our understanding of the underlying mechanisms (and technologies) which determine its modes of operation. While the liability study already has shed light on the IT infrastructure the underlying mechanisms of interaction between participants have not been fully outlined yet. Identifying and understanding these would help to leverage and manage relevant partners. Since such a project lives on from its members, the collaboration between TechQuartier and FINDER contributes directly to the long-term success of the safeFBDC.

“If we are to make strategic sense of innovation communities, ecosystems, networks, and their implications for competitive advantage, we propose that a new approach to strategy [called] ’open strategy’ is needed.” – Chesbrough and Appleyard, 2007: 58[1]

An important underlying idea of innovation is its reliance on competition and thus the intertwined nature of both innovative and competitive behaviour.[2][3][4][5] While this idea has prevailed for a long time the predominance of competition has been slowly losing ground to the idea of cooperation.[6] In that light the concept of business ecosystems gains in prominence in both research as well as its application in business. Before diving into the underlying mechanisms of ecosystems we first should line out what we can understand under such a concept.

Back in school ecology taught us that ecosystems are systems of living and non-living interacting components within the same environment. So how can we apply that concept to business? An innovative reader (as innovation is also the application of an established idea to a new context[7]) may think about something in the line of the following:

“Business ecosystems are a network of firms with differing interests bound together as a collective whole such that the fate of its members is bound to the structure of that network and the roles played by its members.” – Tan, Tan & Oh, 2007: 2[8]

In case of the safeFBDC the set of goals, its mission defined by its value proposition, binds together the consortium. The distinction is an open approach of formulating the mission – in other words their strategizing. That openness allows cooperation, a joint engagement in a strategy process of different organizations instead of their competition.[9] Following the literature, we can therefore define the safeFBDC as an ecosystem-as-structure.[10] For such structural approaches of ecosystems a keynode member with central positioning is of importance.[11] Such keynode members, already generally addressed in a blogpost by my colleague James, have three major tasks.

They consolidate disperse resources & capabilities, as e.g. knowledge, of members.

They engineer processes to initiate and grow the ecosystem.

They oversee the creation and extraction of value for members.[12]

Therefore, the first research project to be conducted will be to identify if and how the TechQuartier is fulfilling the role of an orchestrator for the safeFBDC. A network analysis will be conducted in the first step. The results – the existing ties within the ecosystem – coupled with the second step, a cluster analysis of the activities carried out, should therefore determine the TechQuartiers role as orchestrator.

With that in mind we can have a look on how the mode of operation leads to the realization of the projects objectives, namely the development of AI applications. Instead of competition the project allows the collaboration in the provisioning and usage of shared, aggregated and uniformly formatted, cross-sectoral financial data. Such a concept of open strategy offers advantages for both affiliated producers and consumers.[13] Typically benefits for producers are lowered development and launch costs, quality improvement due to a joined development environment and increased speed to market. This, in turn, translates into the benefits of consumers since the reduced costs are reflected in the price (up to being open source) as well as a direct incorporation of feedback and implementation of specifications in the development cycle.[14] Since for the safeFBDC participants are often both – provider and user of data – an open strategy, triggered by the access to data, is of high functionality.

However, there also loom disadvantages which need to be tackled. In my GAIA-X post I already highlighted the loss of established business models and hence value appropriation. Accordingly, participants engaging in cooperation within an ecosystem have to find new ways to appropriate value within the value chain to generate profit.[15][16] Data monetarisation therefore is a research object of special interest to us. Hence, building on our first research project we will investigate how the TechQuartier, in its role of orchestrator, can determine and govern a value appropriation regime.

Together, Luisa Kruse and me are looking forward to report on our progress on both research projects in the upcoming months.

[1] Chesbrough, H. W., & Appleyard, M. M. (2007). Open innovation and strategy. California management review, 50(1), 57-76.

[2] This is based on Schumpeters (1934, 1939, 1950) work who expected that innovative behaviour is based on the profit expectations during the growth of an industry as the major determinants of a firms growth.

[3] Schumpeter, J. A., & Nichol, A. J. (1934). Robinson’s economics of imperfect competition. Journal of political economy, 42(2), 249-259.

[4] Schumpeter, J. A. (1939). Business cycles (Vol. 1, pp. 161-174). New York: McGraw-Hill.

[5] Schumpeter, J. A. (1950). The march into socialism. The American Economic Review, 40(2), 446-456.

[6] McKinsey and Company, 2015, Global Media Report

[7] Martín‐de Castro, G., López‐Sáez, P., Delgado‐Verde, M., Quintane, E., Casselman, R. M., Reiche, B. S., & Nylund, P. A. (2011). Innovation as a knowledge‐based outcome. Journal of knowledge management.

[8] Tan, F. T., Ondrus, J., Tan, B., & Oh, J. (2020). Digital transformation of business ecosystems: Evidence from the Korean pop industry. Information Systems Journal, 30(5), 866-898.

[9] Gooyert, V. D., Rouwette, E. A. J. A., & van Kranenburg, H. L. (2019). Interorganizational strategizing.

[10] Adner, R. (2017). Ecosystem as structure: An actionable construct for strategy. Journal of management, 43(1), 39-58.

[11] Spigel, B. (2017). The relational organization of entrepreneurial ecosystems. Entrepreneurship Theory and Practice, 41(1), 49-72.

[12] Dhanaraj, C., & Parkhe, A. (2006). Orchestrating innovation networks. Academy of management review, 31(3), 659-669.

[13] Chesbrough, H. W., & Appleyard, M. M. (2007). Open innovation and strategy. California management review, 50(1), 57-76.

[14] Appleyard, M. M., & Chesbrough, H. W. (2017). The dynamics of open strategy: from adoption to reversion. Long Range Planning, 50(3), 310-321.

[15] Hautz, J., Seidl, D., & Whittington, R. (2017). Open strategy: Dimensions, dilemmas, dynamics. Long Range Planning, 50(3), 298-309.

[16] Chesbrough, H., Heaton, S., & Mei, L. (2020). Open innovation with Chinese characteristics: a dynamic capabilities perspective. R&D Management.

Whereas FinTechs and digital financial applications are labeled “disruptive forces” and “game changers” shaking up the existing world of finance and beyond within industry and even politics, academics tend to hold the view that by a bare change of the platform or transaction setting of our financial decisions, existing theoretical frameworks are not challenged too intensively.

However, not only does digitalization allow for more collaboration – between humans, distributed humans as well as between humans and technological entities – but also for different ways of collaboration. Imagine you consider buying Apple stocks in four different situations:

i) Analyzing your finances, you consider you are liquid enough now to invest and Apple seems a solid start for that. You open your online depot and fulfil the transaction.

ii) When opening your interactive depot, you just saw your boss sold his 120 Apple stocks just a minute ago. You still continue your transaction?

iii) When opening your online depot which you share with your baseball mates, you need to get the majority of them on board before the buying trade is possible. Do you consider researching a bit more? Are your mates going to agree to this transaction?

iv) While surfing on your phone, a push-up from your online trader pops up – their chatbot informs you it is a good time to buy Apple stocks now. Do you follow this advice on the go?

Considering these, a mere selection of possible scenarios of a trading situation, it becomes obvious that human financial decisions are shaped through contact, if online or offline, direct or indirect, if in the form of advice, communication or the pure existence of a social group within which an individual makes a decision. Keeping in mind the vast financial and strategic decision-making literature on nudges with the numerous examples of how framing a decision context changes our decisions, FinTech applications with their diverse setups, designs and defaults are definitely worth having a second glance from an academic perspective. FinTech applications give a new angle to financial decision-making transforming the way of collaboration. Does online and task-related communication such as in a collaborative investment app free individuals from halo effects? Does advice from AI remove or strengthen critical thinking? It remains the joint task of practitioners and academics to understand and design these applications as frames for inclusive, unbiased decisions so that research can serve its purpose – society.